On 11 April 2024, the Home Office implemented the most significant shift in family migration policy in a decade, raising the income threshold to £29,000. For many applicants, this change turned a straightforward process into a source of intense anxiety regarding the uk visa financial requirements 2025. You’re likely aware that even a minor technical error in your financial evidence can lead to a costly refusal. It’s frustrating to face these shifting goalposts, especially when the Immigration Health Surcharge has already climbed to £1,035 per year for most adult applicants.

We believe that your path to the UK should be defined by professional precision rather than luck. This expert guide helps you master the £29,000 minimum income requirement and shows you exactly how to evidence your finances to secure your UK visa with absolute confidence. We’ll provide a clear eligibility breakdown and a comprehensive list of documents that meet OISC standards to ensure your application is robust from the start. By the end of this article, you’ll have a definitive roadmap to navigate the current policy freezes and planned increases with total clarity.

Key Takeaways

- Understand the strategic implications of the £29,000 minimum income requirement and how the 2025 policy freeze impacts your family’s immigration roadmap.

- Learn how to navigate the complex uk visa financial requirements 2025 by correctly categorising your income sources and adhering to the mandatory six-month evidentiary rules.

- Discover how to utilise the £88,500 cash savings threshold as a robust alternative to income, including the precise holding requirements and property sale exceptions.

- Identify potential exemptions through the “Adequate Maintenance” test to determine if specific UK benefit receipts allow you to bypass the standard financial thresholds.

- Minimise the risk of a technical refusal by mastering the “Specified Evidence” regulations and the critical 28-day rule for all submitted financial documentation.

Understanding the UK Visa Financial Landscape in 2025 and 2026

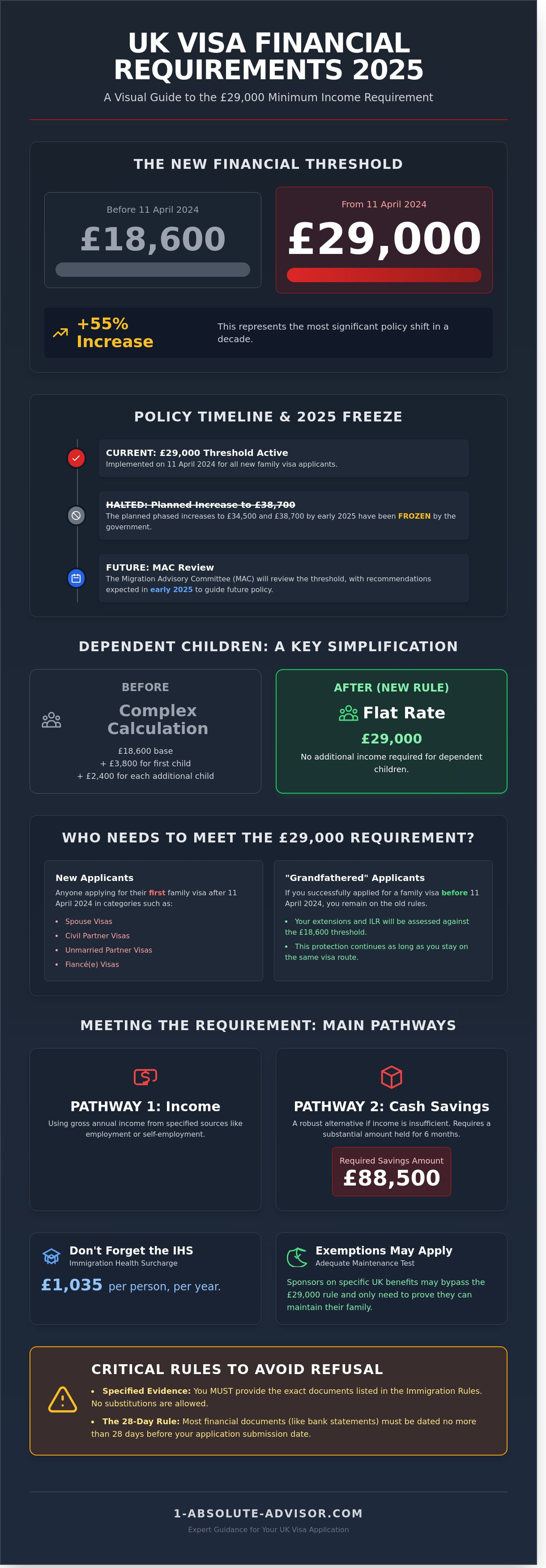

The UK’s immigration framework underwent a seismic shift on 11 April 2024. Before this date, the Minimum Income Requirement (MIR) for spouse and partner visas stood at a stable £18,600. Current regulations now demand a gross annual income of at least £29,000 for most applicants. This change represents the first stage of a multi-part adjustment designed to ensure that families are self-sufficient. For those planning their future, understanding the UK immigration policy overview is essential to see how these financial mandates align with broader border controls. These uk visa financial requirements 2025 reflect a move toward higher economic thresholds for residency.

Strategic planning is now more critical than ever. The Migration Advisory Committee (MAC) is currently conducting a full review of these thresholds, with recommendations expected in early 2025. This review will likely dictate whether the current stability remains or if further adjustments are necessary for 2026. Applicants must stay informed about these developments to avoid unexpected hurdles. One positive development involves dependent children. Previously, each child required an additional financial buffer of £3,800 for the first child and £2,400 for each subsequent child. Under the new £29,000 rule, this extra burden has been abolished. This simplification allows families to focus on meeting a single, flat threshold regardless of the number of children involved.

- The current MIR is fixed at £29,000 per annum for new applicants.

- The 2024 hike from £18,600 was a 55% increase in the baseline requirement.

- Dependent child supplements no longer apply to the £29,000 threshold.

- The MAC 2025 review will determine future policy shifts for the 2026 period.

The 2025 Policy Freeze: Why the £38,700 Threshold Was Halted

The previous government intended to raise the MIR to £34,500 and eventually £38,700 by early 2025. However, the Labour government announced a strategic freeze in July 2024. This decision keeps the threshold at £29,000 for the foreseeable future. It’s a vital window for applicants. It provides a level of predictability that was missing during the volatile policy shifts of early 2024. While the income requirement is frozen, applicants shouldn’t ignore other costs. The Immigration Health Surcharge (IHS) rose to £1,035 per year in February 2024 and remains at this elevated level. This stability in the income threshold allows for more precise long-term financial forecasting for families.

Who Does the £29,000 Requirement Apply To?

The £29,000 threshold applies to most family-based routes. This includes Spouse visas, Civil Partner visas, Unmarried Partner visas, and Fiance visas. The 11 April 2024 date is the critical divider. If you applied for your first visa in one of these categories before this date, you’re “grandfathered” under the old £18,600 rules. This protection extends to your extensions and permanent residency applications. New applicants entering the system for the first time after 11 April 2024 must meet the higher £29,000 standard. Meeting the uk visa financial requirements 2025 is mandatory for all new entries into the family migration system. The rules are strict. Even a small shortfall can lead to a refusal, making professional assessment of your income sources vital.

Calculating Your Income: The Five Primary Categories

The Home Office evaluates every application through a strict framework of seven categories, labelled A through G. Understanding which category fits your specific situation is the first step in meeting the uk visa financial requirements 2025. Mistakes here often lead to immediate refusals, as caseworkers follow the official Home Office financial requirement guidance with zero flexibility for missing evidence. You’re expected to provide a perfect paper trail that aligns exactly with one of these pre-defined routes.

One primary rule determines whose income you can actually use. If you’re applying from outside the UK, only the British sponsor’s income counts toward the threshold. The applicant’s overseas earnings are disregarded entirely. However, if the applicant is already in the UK with valid permission to work, you can combine both salaries to reach the target. This distinction catches many couples off guard during the initial planning phase, often requiring the sponsor to secure a higher-paying role before the process can begin.

Category A vs. Category B: Salaried Employment Explained

Category A is the most common route for those who’ve been with their current employer for at least six months. The Home Office calculates your annual income based on the lowest gross monthly salary received during that period. If you earn £3,500 one month but £3,100 the next due to unpaid leave, they’ll multiply the £3,100 by 12. Non-salaried income, such as hourly wages, is handled differently; caseworkers take the mean average of the last six months and annualise it to check if you meet the uk visa financial requirements 2025.

Category B serves those who’ve changed jobs recently or have fluctuating earnings that don’t meet the “lowest point” rule of Category A. Category B requires a two-part assessment where you must prove you’re currently earning the required threshold and have also earned that total amount in the 12 months prior to your application date. This route requires 12 months of payslips and bank statements rather than six, doubling the administrative burden on the applicant.

Self-Employment and Director Income (Category F and G)

Self-employed individuals and directors of specified limited companies face the highest level of scrutiny. Category F relies on the last full financial year, while Category G allows you to use an average of the last two financial years. This is often necessary if your business had a temporary dip in one year but performed strongly in the other. You’ll need to provide HMRC documents like the CT600 or SA302 to verify every pound claimed, alongside business bank statements that match the accounts exactly.

For many directors, the primary challenge isn’t just documenting income, but ensuring the business generates enough revenue to comfortably meet the threshold. If your B2B company needs to strengthen its sales pipeline to build a more robust financial profile for your application, you can check out Virtual Sales Limited for strategic guidance.

For company directors, managing the finances required for both visa applications and corporate tax liabilities (like the one documented in a CT600) can be complex. Specialist brokers such as V4B Business Finance can provide funding solutions to help businesses meet their tax obligations smoothly.

Timing is everything when it comes to business income. You must ensure your application is submitted within nine months of your company’s financial year-end to ensure the data is considered “current” by the Home Office. If your accounts are dated 31 March 2024, you must apply before 31 December 2024 to use those figures. If you’re unsure about your eligibility or the strength of your documentation, consulting a strategic advisor can prevent costly delays in your relocation plans. It’s better to delay an application by a month to gather better evidence than to risk a refusal on a technicality.

Using Cash Savings to Meet the Financial Requirement

For many applicants, demonstrating a steady annual salary isn’t always feasible. The uk visa financial requirements 2025 allow for significant flexibility through the use of cash savings. If you choose to rely solely on savings to meet the threshold without any supplementary income, the required amount is currently £88,500. This figure stems from the updated minimum income requirement of £29,000 established in April 2024. Relying on savings provides a level of certainty for those who might not meet the strict employment criteria but possess substantial personal capital.

Home Office mandates state that these funds must have been under your control for at least six months prior to the application date. This 182-day rule ensures the money isn’t a temporary loan intended to artificially inflate your financial standing. There’s a vital exception for those who’ve liquidated assets; if you sell a property or receive an inheritance within that six-month window, you can use the cash immediately. You must provide a clear audit trail, such as land registry documents or a solicitor’s letter. Gifted money is also permitted, provided it’s a genuine gift with no obligation to repay. A signed declaration from the donor is essential to confirm the funds are yours to keep, preventing “recycled” funds from being used across multiple applications.

Using savings is particularly advantageous for self-employed individuals or those with seasonal contracts. It provides a stable buffer that compensates for months where earnings might dip below the pro-rata requirement. Detailed analysis from the House of Commons Library regarding the partner visa financial requirements highlights how these thresholds have evolved to ensure families can support themselves without relying on public funds. Understanding these nuances is vital for anyone navigating the uk visa financial requirements 2025 to ensure their application isn’t rejected on technical grounds.

The Formula for Combining Income and Savings

You can combine savings with employment income to bridge a shortfall. Current regulations ignore the first £16,000 of your savings because this is the threshold at which most means-tested benefits cease. The remaining balance is divided by 2.5, reflecting the 30-month duration of the initial visa. The exact calculation is: (Total Savings – £16,000) divided by 2.5 equals the income offset. A practical example of this is: if you earn £20,000, you need £38,500 in savings to bridge the £9,000 gap.

Permitted Sources of Cash Savings

Funds must be held in a regulated financial institution and be instantly accessible. Acceptable accounts include standard current accounts, savings accounts, and ISAs. You can’t use “locked” investments like certain pension schemes or stocks that haven’t been liquidated into cash. The money can be held in the name of the applicant, the sponsor, or both as a joint account. If the funds are in an overseas account, the bank must be on the Home Office’s list of approved institutions, and the balance will be converted to GBP using the OANDA exchange rate on the date of application.

Exemptions and the Adequate Maintenance Test

While the standard Minimum Income Requirement (MIR) serves as the primary benchmark for most applicants, the UK immigration system provides a specific safety net for sponsors who receive certain state benefits. This pathway bypasses the fixed £29,000 threshold, replacing it with the “Adequate Maintenance” test. It’s a recognition by the Home Office that individuals with disabilities or significant caring responsibilities may not have the same earning capacity as other sponsors, yet they still possess a right to family life.

This alternative route doesn’t mean the financial scrutiny is less intense. In fact, the evidentiary burden often increases because you must prove that the family can live above the poverty line without additional recourse to public funds. Meeting the uk visa financial requirements 2025 through this method requires a meticulous breakdown of weekly income against essential living costs. We often see applicants struggle not because they lack funds, but because they fail to document their “surplus” income with the precision required by entry clearance officers.

List of Qualifying Benefits for Exemption

To qualify for this exemption, the sponsor, not the applicant, must be in receipt of at least one specific benefit. The Home Office updated this list to reflect changes in the social security landscape, including the 2025 inclusion of modernised Scottish welfare payments. The qualifying benefits include:

- Carer’s Allowance or Attendance Allowance.

- Personal Independence Payment (PIP) and Disability Living Allowance (DLA).

- Adult Disability Payment (ADP) or Child Disability Payment in Scotland.

- Industrial Injury Disablement Benefit or Severe Disablement Allowance.

- Armed Forces Independence Payment or Guaranteed Income Payment under the Armed Forces Compensation Scheme.

The sponsor’s status as a recipient must be current at the time of application. You’ll need the most recent DWP annual uprating letter or a confirmed statement of entitlement to validate this claim.

How to Calculate Adequate Maintenance

The Home Office uses a specific formula to determine if your finances are sufficient. It’s a three step process that leaves no room for estimation.

Step 1: Calculate your total net weekly income. This includes the sponsor’s benefits, any employment income from the sponsor or the applicant (if they’re already working legally in the UK), and any other permitted income sources.

Step 2: Deduct your weekly housing costs. This must include your full rent or mortgage payment plus your Council Tax. For example, if your monthly rent is £800 and Council Tax is £150, your weekly housing cost is roughly £219.23.

Step 3: Compare the remaining figure against the relevant DWP Income Support rate for a family of your size. For 2024/25, the rate for a couple is £142.25 per week. If your net income after housing costs is £142.26 or more, you technically meet the requirement.

To satisfy the Home Office guidance, the applicant must demonstrate that their weekly income, after deducting all housing costs, results in a surplus that is at least equivalent to the current DWP cash payment for a family of their specific size.

Accuracy is the foundation of a successful application under these rules. If you’re unsure how your specific benefit package fits into the uk visa financial requirements 2025, professional oversight is essential.

Contact our specialist advisors for a detailed financial assessment of your spouse visa eligibility.

Strategic Evidence Preparation: Avoiding Common Refusals

Caseworkers at the Home Office operate under the “Specified Evidence” rule defined in Appendix FM-SE. This isn’t a flexible guideline; it’s a rigid framework where the absence of a single monthly bank statement or a missing payslip results in an immediate refusal. Statistics from recent years indicate that approximately 15% of family visa refusals stem from technical document errors rather than a genuine lack of income. Precision is the only way to guarantee a successful outcome.

The “28-day rule” remains the most frequent point of failure for applicants. Every financial document, including the mandatory employer’s letter and the most recent bank statement, must be dated no earlier than 28 days before the online application submission date. If your final bank statement is dated 1st June but you don’t hit the “submit” button until 30th June, your evidence is technically expired. This single day of overlap often separates a successful uk visa financial requirements 2025 submission from a costly and stressful rejection.

As the Home Office transitions toward fully digital systems for 2026, the organisation of your evidence bundle is paramount. Applicants should scan and upload documents as clear, searchable PDFs. Using a logical naming convention, such as “01_Bank_Statement_Jan_2025.pdf”, assists the caseworker in navigating your file. A legal cover letter serves as the essential narrative for this bundle. It doesn’t just list documents; it explains them. If you’ve changed jobs or received a pay rise during the six-month period, the cover letter “narrates” these transitions to ensure the caseworker follows the logic of your financial eligibility without confusion.

The Document Checklist: Bank Statements and Payslips

Every payslip must align perfectly with a corresponding entry on your bank statement. If a payslip indicates a net pay of £2,450 but the bank deposit shows £2,400 due to a minor deduction, you must provide a written explanation. Internet bank statements are a common trap. The Home Office typically rejects simple PDF downloads unless every page is either stamped by the bank branch or accompanied by a formal letter on headed paper confirming the statements’ authenticity. Consistency across all dates and figures is the absolute standard required for approval.

Why Professional OISC-Registered Advice is Critical

Technical errors are the primary driver of visa delays and denials. A professional “Document Checking Service” provides a final safety net to identify gaps in your uk visa financial requirements 2025 evidence before you commit to the non-refundable application fees. Expert advisors at 1 Absolute Advisor identify complex “Category” overlaps, such as combining dividend income with salaried work, which require specific calculations that often elude DIY applicants. You can secure a professional eligibility assessment to verify that your documentation meets the current £29,000 threshold and adheres to the latest Home Office internal guidance.

Taking a proactive approach to evidence preparation isn’t just about gathering papers; it’s about building a bulletproof case. By adhering to the 28-day rule and ensuring every transaction is accounted for, you remove the element of caseworker discretion. This level of diligence ensures your family’s future in the UK is built on a foundation of absolute compliance and professional integrity.

Securing Your UK Residency Amidst Shifting Financial Standards

Navigating the uk visa financial requirements 2025 demands more than just a healthy bank balance; it requires a meticulous alignment of your financial history with strict Home Office categories. Whether you’re relying on the £29,000 minimum income threshold for family routes or calculating complex self-employment earnings under Category F, the margin for error is non-existent. Home Office statistics consistently highlight that evidentiary oversights remain a leading cause of avoidable refusals, making the strategic preparation of your 6-month or 12-month financial statements a critical priority for every applicant.

Our London-based team of OISC-registered immigration consultants brings a holistic, strategic perspective to your case. We’re specialists in complex Spouse and Skilled Worker visa applications, ensuring every document meets the exact technical standards required by the current rules. We don’t just process paperwork; we act as your strategic partners to mitigate risks before they surface. You’ll benefit from our national coverage and a commitment to professional integrity that places your future on certain ground.

Book a Fixed-Fee Visa Consultation with our London Experts to ensure your application is built on a foundation of absolute compliance. Your successful transition to life in the UK is within reach when you have the right professional expertise by your side.

Frequently Asked Questions

Can I combine my income from two different jobs to meet the £29,000 requirement?

You can combine income from multiple jobs held by the sponsor to reach the £29,000 threshold. If you’re already in the UK on a valid visa with work rights, you can also include your own earnings. It’s essential that both roles meet the specific evidentiary requirements, such as having 6 months of continuous payslips for each position under Category A.

What happens if my sponsor’s income drops below £29,000 after we apply?

The Home Office assesses your financial eligibility based on the evidence provided at the exact time of your application submission. If your documents prove you met the requirement when you paid the fee, a subsequent salary drop won’t typically lead to a refusal. We suggest maintaining your financial records carefully until a decision is reached to ensure total compliance with the rules.

Do I need to show extra income if I am bringing my children to the UK?

Under the rules effective from 11 April 2024, you don’t need to show additional income for dependent children. The financial requirement is now a flat £29,000 regardless of the number of children included in the application. This change simplified the previous system where the threshold increased by £3,800 for the first child and £2,400 for each subsequent child.

Can I use a gift from my parents as cash savings for the visa?

You can use gifted funds from parents, but the money must have been in your personal bank account for at least 6 months before applying. You’ll need a signed declaration from your parents confirming the money is a gift, not a loan, and that they’ve no legal claim to it. This ensures the Home Office views the funds as being under your absolute control.

How far back do my bank statements need to go for the financial requirement?

Your bank statements must cover at least 6 months if you’re using salaried income under Category A to meet the uk visa financial requirements 2025. If you’re relying on self-employment or Category B, you’ll need 12 months of records. Every statement must be original or certified by the bank; the Home Office won’t accept simple online screenshots or partial transaction histories.

Is the Immigration Health Surcharge (IHS) part of the financial requirement?

The IHS is a separate mandatory fee and isn’t included in the £29,000 income calculation. Since 6 February 2024, the surcharge is £1,035 per year for each adult applicant. For a standard 33-month spouse visa, you’ll need to pay £2,846.25 upfront. This payment is non-negotiable and provides you with access to the National Health Service during your stay.

Can I use rental income or dividends to meet the UK visa threshold?

Rental income and dividends are valid sources of non-employment income for the uk visa financial requirements 2025. To use these, you must provide 12 months of evidence, including tax returns and proof of property ownership or share certificates. Combining these with a salary is possible, but the documentation must be precise to show the income is stable and legally declared.

What is the “28-day rule” regarding visa financial evidence?

The 28-day rule dictates that your most recent financial document, like a payslip or bank statement, cannot be older than 28 days from your application date. If your evidence falls outside this window, the Home Office will likely reject the application for being outdated. It’s a strict deadline that requires careful strategic planning to ensure your submission is compliant and successful.